The Grid Can’t Keep Up – Opportunities for Technology Vendors in Energy

By: Jeff Klemens, William Kunin, Siddhi Chandak, Sasha Pasmanik

Energy Demand is Compounding

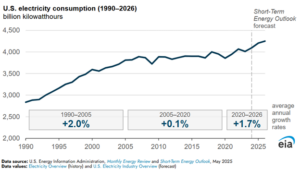

U.S. electricity demand was essentially flat from 2005 – 2020 with annual consumption growing at +0.1%. That era is over. The U.S. Energy Information Administration (EIA) expects U.S. electricity use to grow 1% in 2026 and 3% in 2027.

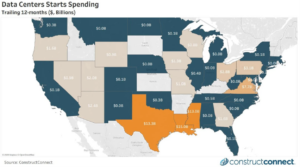

The relatively strong growth is driven by increasing demand from data centers. There were $78 billion in new data center construction starts in 2025 (190% yoy growth), and $25 billion in construction starts in January 2026 alone per ConstructConnect.

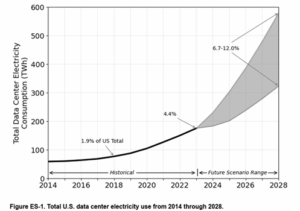

In 2018 data centers consumed 1.9% of total annual U.S. electricity consumption. In 2023 consumption increased to 4.4% and the Berkeley Lab expects usage to represent anywhere from 6.7% to 12.0% by 2028.

Source: Berkeley Lab 2024 United States Data Center Energy Usage Report

Similarly, Goldman Sachs Research estimates global power demand from data centers to increase 165% by 2030 (relative to 2023). They believe this power demand from data centers will likely require $720 billion in additional grid investment through 2030.

Grid operators are already warning that without significant upgrades, overloads are inevitable. The energy industry needs to address growing demand by: 1) Building more generation capacity, 2) Improving efficiency across existing infrastructure, and 3) Optimizing how energy is priced, traded, and delivered. Software and tech-enabled services can help with all three. Utilities need better demand forecasting to plan capacity additions, project developers need tools to navigate compliance requirements, and market participants need automated systems to capture value in volatile markets.

Vendors Emerging to Support the Energy Lifecycle

In addition to rising energy demand, much of the work across the energy stack remains highly manual and fragmented. Bid submissions, project compliance and meter data reconciliation is still run through spreadsheets, email chains and disconnected legacy systems. As we enter a period of higher volume and increasing regulatory complexity, these manual processes become further strained. This dynamic is creating opportunities for technology vendors spanning the full operational lifecycle of how energy is financed, built, traded, and delivered. While there are several large incumbents and numerous upstarts serving this market, we have highlighted five below. Disclaimer: Sageview is not an investor in any of these businesses

It starts with market intelligence. Arcobi (formerly Arcus Power) has built an energy intelligence platform on top of 25 years of North American power market data. The company leverages AI to forecast prices, demand, and coincident peaks (highest point of energy consumption on a grid at any given time). Predicting energy demand is extremely important for utility companies and energy managers. The insights are also utilized by energy traders and independent power producers (IPPs).

On the project development side, Euclid Power combines software and technical expertise to support the renewable energy project lifecycle (including development, investment, and construction). Euclid has facilitated over $10 billion in renewable energy investments across 1,000+ projects and 12+ gigawatts of capacity (enough to power ~9 million American homes). Euclid replaces a patchwork of spreadsheets, lost emails, and disorganized data rooms with a structured platform that shrinks weeks of work into days.

As those projects move toward construction and operation, compliance can become a bottleneck. Empact Technologies has built an AI-native platform, called NexusIQ to manage renewable energy project compliance. Empact manages compliance for Investment Tax Credits and Production Credits, ensuring developers meet prevailing wage, apprenticeship, and domestic content requirements. The company currently has more than $3 billion in tax credit value under engagement and delivers immediate ROI for developers, engineering firms, and tax credit investors.

For those participating in the wholesale electricity market, Hartigen’s PowerOptix platform acts as the system of record between a power producer’s physical assets and the financial elements of selling electricity. Power generators and energy traders are submitting bids / offers, ingesting meter data, settling transactions and managing compliance requirements (e.g. Federal Energy Regulatory Commission regulations) every day. Hartigen allows energy market participants to perform all of these actions from a single platform.

When energy reaches the end user, the physical grid itself needs monitoring. Whisker Labs has deployed over 1.2 million Ting sensors that analyze 30 trillion electrical measurements per second, using AI to detect dangerous arcing and grid faults before they cause fires. The platform serves both insurance carriers looking to reduce catastrophic loss and utilities seeking real-time grid intelligence.

Why Sageview is Paying Attention

At Sageview, we look for technology companies solving mission critical operational problems in markets with increasing complexity. Structural energy grid strain (data center build outs), increasing regulatory burden (tax credits, FERC regulations) and a shift towards automated workflows (away from manual spread sheet driven processes) is fostering an environment for durable technology vendors. The five companies profiled are not competing with each other, but instead building the next generation infrastructure to power the energy market. We believe this space is worth watching closely and we’re energized to actively explore opportunities.

See more at our Substack

Disclaimer: For informational and educational purposes only; not investment advice